Types of Financial Statements with Explanation

Financial statements are very important for any organization. Because these statements show a fair and true condition of how the organization financially performed in the last financial period and the actual financial position of the organization. Any organization whether profit or non-profit who has financial transactions prepare these statements. The forms of these statements can be different. These statements are an important part of an annual report of any organization. A business entity’s management, staffs, investors, shareholders, major suppliers, major customers, stock exchanges, government authority, and other related stakeholders use these financial statements.

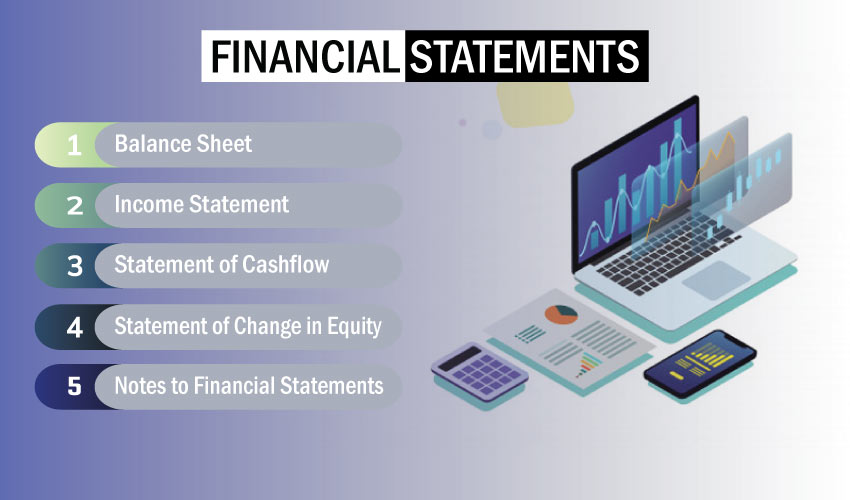

Types of Financial Statements

There are basically three types of financial statements. But two other crucial parts of the annual report are also considered as financial statements. So, generally financial statements are of five types:

- Balance Sheet

- Income Statement

- Statement of Cashflow

- Statement of Change in Equity

- Notes to Financial Statements

Each of the types is explained below:

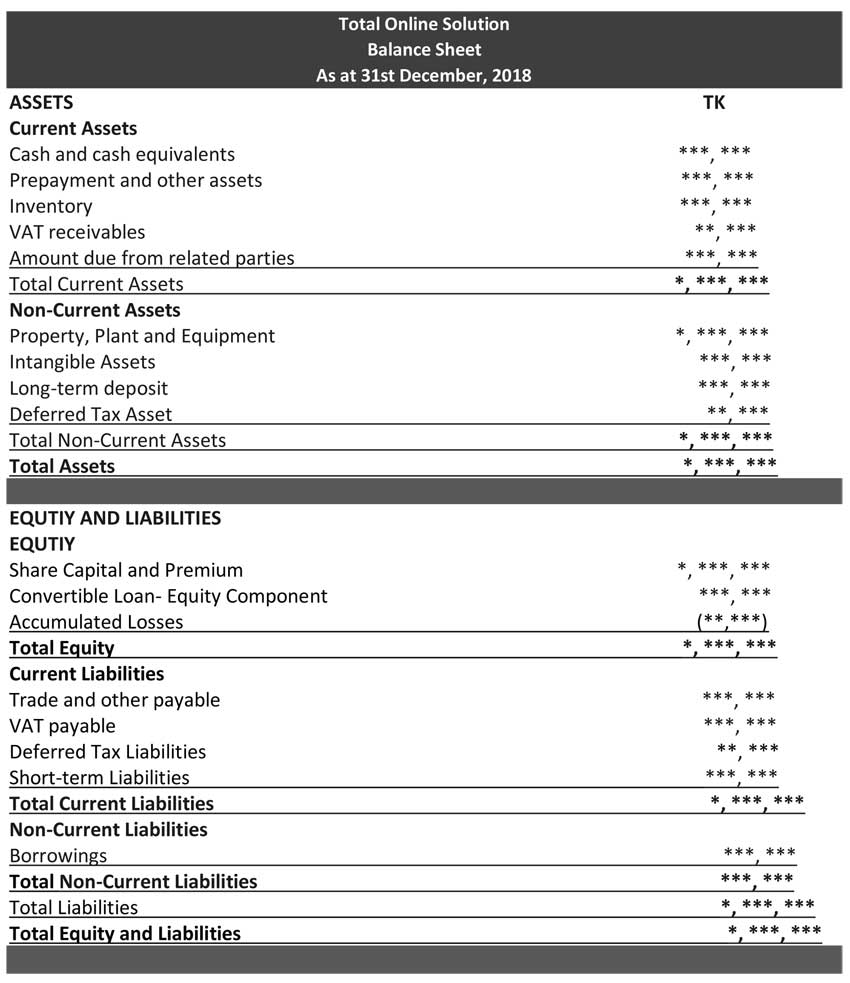

Balance Sheet

Statement of financial position is another name of the balance sheet. Because you can get the net worth of the entity if you remove total liabilities from total assets. It records the balances of assets, liabilities and shareholder’s equity at the date of reporting.

Balance Sheet’s accounting equation is, Asset= Liabilities + Shareholders’ Equity

So, the balance sheet’s three main elements are:

- Assets

- Liabilities and

- Shareholders’ Equity

These elements are briefly described below:

Assets:

Economically and legally owned resources by the entity are known as assets. As for example, land, building, money, and cars are assets of any entity. Again, assets can be of two types: Current or Short-term Assets and Non-Current or Fixed Assets.

Current Assets include petty cash, cash on hand, work in progress, raw materials, prepayments, finished goods which can be consumed and converted within twelve months from the date of reporting.

Non-Current or Fixed Assets can be categorized into tangible and intangible. Tangible fixed assets include property, land, equipment, building, long term investments which are expected to be consumed and converted in more than twelve months from the date of reporting. Intangible fixed assets include goodwill, investment, patent, and trademarks.

Liabilities

The obligations that the entity owe to other entity or person are known as liabilities. As for example, bank loan, credit purchases, overdraft, taxes payable, and interest payable. Again, liabilities are classified into two categories: Current or Short-term liabilities and Non-Current or Long-term liabilities.

The obligation which is due within a period of one year. As for example, purchase of any item on credit within five months can be recorded as a short-term or current liability. The obligation which is due within a period of more than one 12 months or one year. As for example, a long-term lease which is due within 3 years can be recorded as a long-term or non-current liability.

Shareholders’ Equity

Shareholders’ equities are different from assets and liabilities. The items that are included in equity are share capital, retained earnings, accumulation of other incomes, preferred stock, and common stock. The changes in assets and liabilities over a period of time will affect the equity’s net value. The equity’s net value can be calculated by subtracting liabilities from assets.

A template of Balance Sheet is given below:

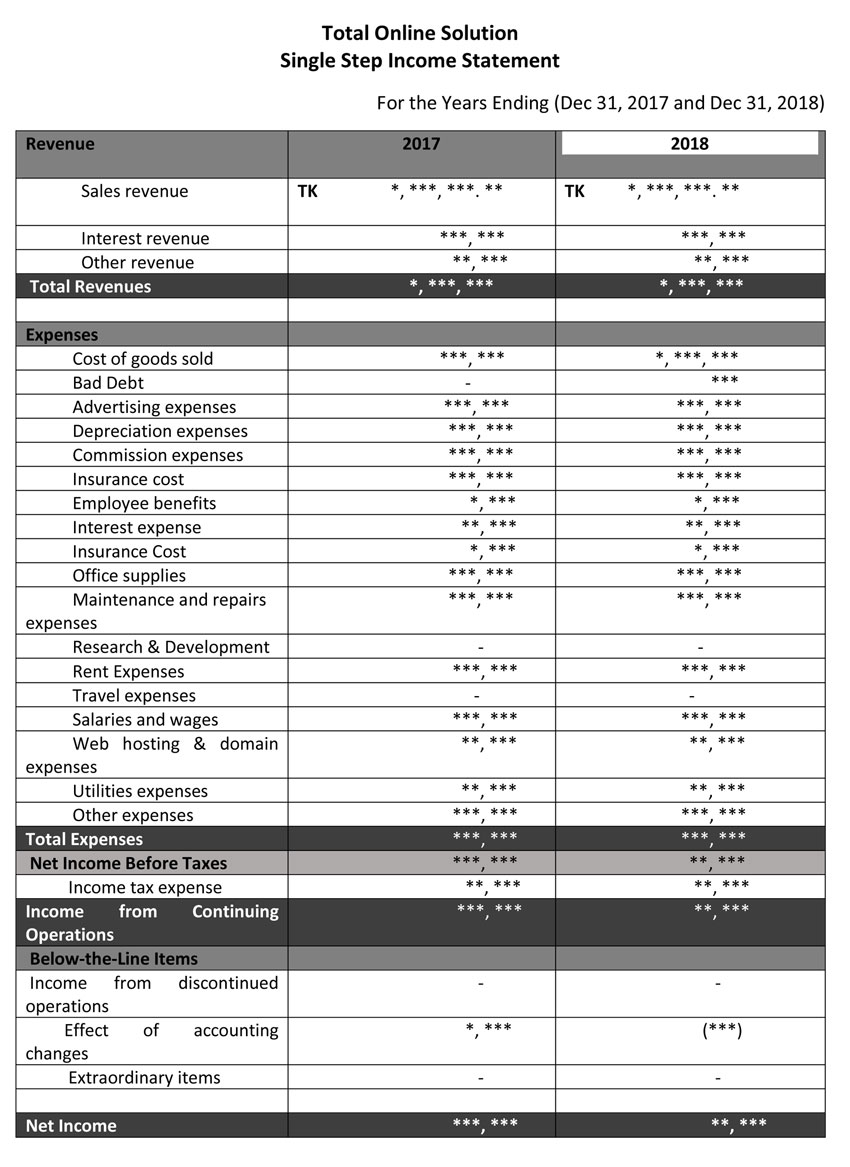

Income Statement

The income statement is a financial statement of an entity reporting three core financial information of the entity for a specific time period. That information includes expenses, revenues, and profit or loss for that time period. Statement of financial performance is another name of the income statement. Because users can measure the entity’s financial performance using this statement from year to year and also compare with its competitors.

Three main elements of the income statement are briefly discussed below:

1. Revenues:

Sales of goods and/or services which an entity makes during a particular accounting period is called revenues. An entity can recognize its revenues either on a cash basis or on an accrual basis. You can have knowledge of how much net sales the entity made in the covered time period from this section.

In the income statement, revenues are normally recorded as a summary. You have to check the provided notes with the income statement for details. You can find the different lines of revenues which the entity has generated during the period from the notes. You can also understand the significance, increase and decline of the different lines of revenues.

2. Expenses:

Operational costs which occur in the entity for a particular accounting period. Salary expenses, depreciation, utilities, transportation expenses, training expenses, interest expenses, and tax expenses are different types of operating expenses. Expenses also include costs of rendering services and goods sold during the particular period. But the costs of goods sold and general and administrative expenses are reported differently.

3. Profit or Loss:

When you deduct expenses from generated revenues, you will get profit or loss. If the generated revenues are greater than the expenses, there is profit. But if the expenses are greater than revenues, there is a loss. Profit or loss will be forwarded to the statement of change in equity and balance sheet.

A template of Single Step Income Statement is given below:

Statement of Cash Flow

It is the financial statement that exhibits the entity’s cash’s movement during a specific period. This statement has three sections: cash flow from 1. operation, 2. investment, and 3. financing activities.

There are various factors which cause net income and cash balance to be fully different. These are noncash adjustments made to net income, investments, changes in working capital, dividend payments, capital inflows and outflows.

Statement of Change in Equity

This financial statement shows equity’s movement, shareholders’ contribution and ending balance of equity at any accounting period. This statement includes total share capital, share capital’s classification, retained earnings, other related state reserves and dividend payments. Statement of Change in Equity is the outcome of the balance sheet and income statement. So, if these two financial statements are prepared correctly, this statement will also be correct.

Notes to Financial Statements

Notes to financial statements are important financial statements about which most of the people forget. International Financial Reporting Standards (IFRS) has made a mandatory requirement that companies have to disclose all the necessary information related to the financial statements for a better understanding of the users. For example, you will find the fixed assets’ balance in the balance sheet, but the details will be available in the notes to the fixed assets.